Banks are expanding passkey login options after a rise in credential theft reports renewed focus on account takeover risks. Financial institutions say passwords remain a weak point because they can be phished, reused across services, or stolen through malware and data breaches. Passkeys aim to reduce those risks by replacing passwords with device-based authentication that is harder to intercept and difficult to reuse outside the legitimate banking app or website.

The rollout is typically positioned as both a security and customer-experience upgrade. With passkeys, users authenticate using a phone’s biometric sensor or a device PIN, avoiding password resets and reducing reliance on one-time codes that attackers can sometimes trick victims into sharing.

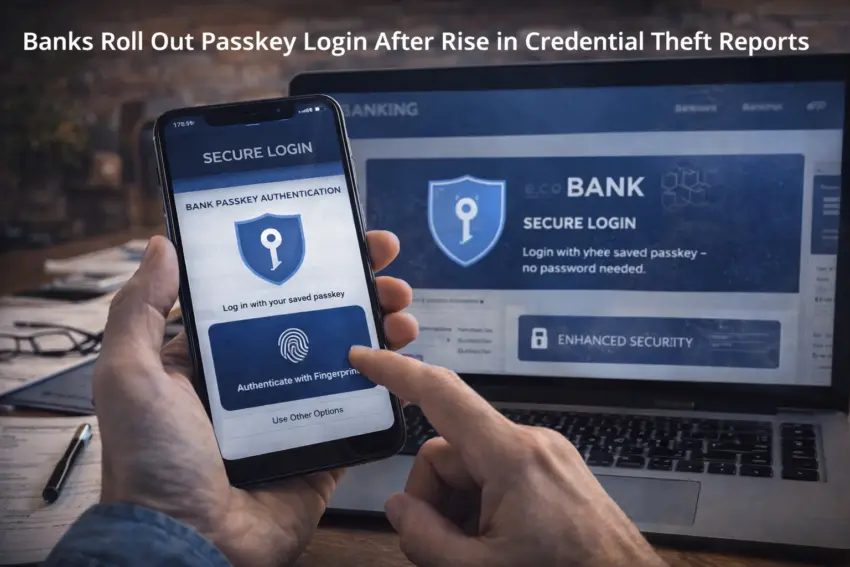

How passkey login works

Passkeys are based on public-key cryptography. A user’s device generates a unique key pair for a specific service. The private key stays on the device and is protected by biometrics or a local PIN, while the bank stores the corresponding public key. During login, the device proves it holds the private key without revealing it—meaning there is no password to steal or type into a phishing page.

In most implementations, the bank’s app prompts the user to approve the login, and the system checks that the request originates from the legitimate service. This design reduces the effectiveness of classic credential phishing, because the passkey will not authenticate on a fake website that does not match the bank’s domain.

Why banks are moving now

Credential theft remains one of the most common entry points for fraud. Attackers use stolen passwords, social engineering, and “phishing-as-a-service” kits to capture logins, then attempt to change account details or initiate unauthorized payments. Banks argue that passkeys remove the most frequently abused secret—the password—and can reduce both fraud losses and support costs linked to password resets and locked accounts.

Another driver is user behavior. Many customers log in primarily on mobile devices, where quick biometric confirmation feels simpler than remembering complex passwords. Banks see that usability advantage as important for adoption.

What customers will notice

When passkeys are enabled, login can become a one-step approval using Face ID, fingerprint, or a device PIN. Depending on the bank, customers may see an option in security settings to “use passkeys,” “enable passwordless login,” or “use device authentication.” In many cases, banks will keep traditional login methods as a fallback during the transition, especially for account recovery.

Limits and remaining risks

Security experts emphasize that passkeys significantly reduce phishing risk, but they do not eliminate fraud. Device compromise, session hijacking, and social engineering can still lead to losses—especially if criminals trick customers into approving actions they do not understand. The strongest systems therefore pair passkeys with transaction confirmation, risk-based checks, and hardened recovery processes.

Account recovery remains a sensitive area. If a bank allows easy recovery through weak channels, attackers may bypass strong login by exploiting customer support or SIM-swap-friendly methods. Banks rolling out passkeys are therefore tightening identity checks and adding more secure recovery options.

“Passkeys take passwords out of the equation, which removes a major target. But recovery and transaction approval still determine how safe accounts really are.”

What banks are adding alongside passkeys

Many institutions are pairing passkeys with additional controls to reduce account takeover and payment fraud:

- Risk-based authentication that increases verification for unusual logins or new devices.

- Device binding to flag attempts to move an account to an untrusted phone.

- Stronger transaction verification for high-value transfers and new payees.

- Improved monitoring to detect abnormal account activity and automated attacks.

- Hardened recovery with stricter identity checks and fewer bypass options.

What happens next

As credential theft remains a major driver of fraud, passkeys are likely to become a default login option for banking apps and web portals. The speed of adoption will depend on clear customer communication, reliable cross-device support, and recovery flows that are secure but still usable. For banks, the shift signals a broader move toward phishing-resistant authentication as a baseline rather than an advanced feature.